The concept of opportunity costs. How do you find the opportunity cost of every decision you make? References in literature

Definition 1

Opportunity cost is an economic term that refers to the loss of benefits (in particular, income or profit) due to the choice of one of the alternative ways the use of various resources and thereby the rejection of other opportunities.

The size of lost profits can be defined as the utility of the most valuable of the excluded alternatives. Note that opportunity costs are an inseparable part of the decision-making process.

From point of view accounting, opportunity costs are not costs, they are only an economic construct for the analysis of lost alternatives.

Von Wieser's opportunity cost theory

Remark 1

The term "opportunity cost" was first introduced by the Austrian economist F. von Wieser in 1914 in his book "The Theory of Social Economy".

Opportunity costs are expressed not only in kind (in goods, the consumption or production of which had to be abandoned), but also in the monetary equivalent of such an alternative. In addition, opportunity costs can be expressed in the form of lost time from the standpoint of its alternative use.

The main provisions of the theory of opportunity costs:

- productive goods represent the future. Their value depends on the value of the final product;

- due to limited resources, competition arises, as well as alternative methods of their use;

- the subjective nature of production costs determines those alternative possibilities that have to be sacrificed in the process of producing any good;

- any thing is characterized by real utility, which is the lost utility of other things that could be produced using the resources spent on the production of this thing (Wiser's law).

The significance of the theory developed by von Wieser for economics is that it was the first to describe the principles efficient production.

Opportunity cost calculation

Remark 2

When calculating opportunity costs, it is necessary to highlight irrelevant costs, which include depreciation, rent, general business expenses, and some general corporate expenses. Irrelevant costs do not change, regardless of the option decision.

For example, when making a decision regarding the release of a new type of product, it is necessary to calculate the costs that the enterprise will incur in the production and sale of this new product, then this value is compared with the expected income from its sale.

On the one hand, it seems quite natural for these purposes to use the calculation of the total cost of the product, multiplied by the planned sales volumes, to obtain the total cost of a new type of product. But this approach misses a key point: a significant proportion of the costs are associated with cash flows that took place even before this decision was made in the past.

Financial management focused on cash flows, which are generated due to the implementation management decisions, makes it possible to calculate opportunity costs based on the planned outflow Money as a result of the adoption this decision. In any case, fixed indirect costs will remain unchanged, so they should not be taken into account opportunity costs.

Investment project efficiency

When calculating performance indicators investment project should take into account only upcoming revenues and costs during the implementation of the project, including those associated with the involvement of previously formed production assets, as well as future losses caused directly by the implementation of the project (for example, from the suspension of existing production due to the organization of a new one in its place).

Previously formed resources used in a new project are evaluated not by the costs of their creation, but by the opportunity cost, which reflects the maximum amount of lost profit associated with the best possible alternative for their use.

Thus, the calculation of opportunity costs is commensurate only with direct costs.

The process of making a managerial decision involves comparing several alternative options with each other in order to choose the best one. The indicators compared in this case can be divided into two groups: the first remain unchanged for all alternative options, the second vary depending on the decision made. It is advisable to compare only the indicators of the second group. These costs, which distinguish one alternative from another, are called relevant. Only they are taken into account when making decisions.

In the process of control, the control system must influence the control object. Actual cash flows, which are reflected in the accounting of the enterprise, act as a result of previously made management decisions. Information about these streams is an element feedback between the subject and the object of control. It has significant value for substantiating management decisions, however, the result of these decisions will be a change not in today's cash flows, but in future ones. To assess the financial and economic efficiency of the managerial decisions made, it is necessary to compare future cash inflows with future cash outflows due to the adoption and implementation of these decisions.

For example, in order to make a decision on the release of a new type of product, it is necessary to calculate the amount of costs that the company will incur in connection with the production and sale of a new product, and compare this value with the expected income from its sale. At first glance, it may seem quite natural to use for these purposes the calculation of the full cost of one product, and, multiplying its amount by the planned sales volume, get overall value new product costs. But this approach overlooks the fact that a significant part of the total cost is associated with cash flows that took place in the past, even before the decision was made. The implementation of the decision will have no impact on the related cash flows in the future. If it is planned to use the stocks of materials already available at the enterprise for the production of a new product, and their quantity is sufficient to cover the entire planned need and no new purchases of these materials are expected, then it is necessary to determine how the costs of purchasing these materials are related to the release of a new product, whether it will reduce the value of these costs, the refusal to produce it, as well as what real cash outflows the enterprise will incur, using these materials in the process of implementing this management decision. Lytnev O.A. Fundamentals of financial management. Part. I: Textbook / Kaliningrad University. - Kaliningrad, 2000.

It can be argued that the material costs for the production of new products for the enterprise will be equal to the amount that it could earn by selling the stock of materials, since the enterprise has no other alternative to using them. A more general definition of economic costs (opportunity costs) refers to them as the payments that the firm is obliged to make, or the income that the firm is obliged to provide to the supplier of resources in order to divert these resources from use in alternative industries. In this example, the release of a new product will be appropriate for the enterprise if the price offered by the buyer for it covers the opportunity costs of both raw materials and materials, as well as all other resources spent on the production of the product.

The make-it-or-buy decision is needed to explore ways best use available production capacity. Solutions could be:

1. Keeping production facilities free;

2. Transition to the purchase of components and the lease of unused funds;

3. Purchase of components and transfer of free capacities to the production of other products.

Producing yourself or acquiring from outside is a task from the field strategic decisions associated with long-term optimization production program. This decision is complex and must be carefully considered and justified. It should be evaluated not only from an economic, but also from a technological, qualitative, and organizational standpoint. At the same time, many conditions must be taken into account: the degree of capacity utilization, the quality of products and services, the creation or reduction of jobs, fluctuations in demand, and so on.

If there is free production capacity, buying from outside is more profitable if the total costs of the acquisition are lower than the variable costs of in-house production.

If a own production involves the expansion of production capacity, it can be opened only if demand is stable and will grow in the future. Otherwise, in the event of a recession market demand capacities become redundant with all the ensuing consequences.

When making this type of decision, there are qualitative relevant factors (important in decision making):

supplier reliability;

supplier quality control;

relationship between employees and administration in the supplier's company;

supplier price stability;

Internal:

capacity ownership;

technological changes.

Another type of similar decision, but in reverse, is to sell or process further, which is associated with the possibility of selling products at a certain stage of production or continuing processing in order to obtain additional income.

Orientation to the cash flows that are generated by management decisions, allows you to define opportunity costs as the amount of cash outflow that will occur as a result of the decision. The decision to launch a new product in production entails a loss of revenue from the sale of materials available at the enterprise. The cost of these materials at the prices of their possible implementation will be the amount of material costs, which are taken into account when substantiating the corresponding decision.

When planning its activities, the enterprise must form such a portfolio of orders so that their totality covers all fixed costs and ensures profit. If this cannot be achieved, then it is necessary to reduce fixed costs that are not directly related to the production and commercial activities of the enterprise. It cannot afford to invest its financial resources into capacity development that does not bring real returns. Anyway we are talking about qualitatively different decisions that have nothing to do with the decision to fulfill a specific order. If the enterprise has a choice, then, of course, one should prefer more profitable option for maximum coverage fixed costs. But the lack of choice cannot be a reason for not producing products whose price is higher than their opportunity cost.

By refusing to produce products that fully cover their opportunity costs in the hope of obtaining more profitable orders that pay for the full cost of each product, the company is missing out on real cash inflows, hoping for expected higher cash inflows in the future. Such behavior is contraindicated in the conduct of business. Business owners (investors) pay their managers the only service - the real increase in invested capital. The manager should not refuse the opportunity to provide at least minimum magnification capital, if it does not have a real alternative opportunity for a more profitable use of the company's assets.

The following forms of practical manifestation of the concept of opportunity costs can be distinguished:

When justifying financial decisions, one should focus primarily on the cash flows that are generated by these decisions. Those and only those cash flows that are directly related to this management decision should be taken into account. Receipts and expenditures of funds, regardless of the time of their occurrence, which are not related to the decision being made, should not be taken into account. In other words, there are incremental cash flows, and the opportunity costs considered in it are marginal. If, as a result of making a decision on the release of new products, it is necessary to hire additional workers, then the marginal cost of maintaining new workers should be included in the cost of the product being mastered, while the cost of maintaining the same size is not relevant to this decision and cannot be included in the opportunity cost.

The decision taken cannot affect the expenses already incurred or the income received earlier. Therefore, justifying this decision, it is necessary to take into account only future cash flows. All past payments and receipts, including the cost of purchasing equipment, are of a historical nature, they can no longer be avoided or prevented.

Projects that generate cash inflows whose present value exceeds the opportunity cost associated with them increase the value of the enterprise. Increasing the capital of owners is the main goal of any enterprise and its managers. It can be said that such an abstract concept of "opportunity costs" gives the manager a powerful, fairly simple, understandable and very practical tool for monitoring the effectiveness of his work: by implementing decisions and projects, cash inflows for which exceed cash outflows, he contributes to the growth of the value of the enterprise, thereby performs its functions in the most appropriate way. This can be formulated somewhat differently: the enterprise should invest only in such projects, the net present value of which has a positive value. The task of the manager is to ensure the selection of just such projects and solutions. Lytnev O.A. Fundamentals of financial management. Part. I: Textbook / Kaliningrad University. - Kaliningrad, 2000.

The application of the concept of opportunity costs poses serious challenges for the management information subsystem. It is obvious that the data of traditional accounting alone is not enough in this case. There is a need to create an accounting system focused on a more complete and accurate identification of opportunity costs - a management accounting system. The cornerstone of such a system is the division of all expenses of the enterprise into conditionally fixed and variable parts in relation to the volume of output (sales) of products. Planning and accounting for costs in this context allows you to more closely link them with the consequences of specific management decisions, to exclude the possibility of "overlapping" on financial results of this decision, the influence of factors not related to it (for example, general factory overheads). Another distinguishing feature of such systems is the wide coverage of enterprise costs by rationing. This allows you to more accurately predict future cash inflows and outflows. The third feature of management accounting systems is the personification of information, that is, the linking of accounting objects with the areas of responsibility of specific managers, which makes it possible to even more clearly delimit the costs that depend on specific decisions from all other costs that are not related to it.

The listed features are reflected in such accounting systems as the normative method of accounting for production costs (standard-cost system), accounting for variable costs(direct costing), accounting by cost centers, as well as profit centers and responsibility centers.

On the Russian enterprises all these systems take root rather slowly, despite the fact that the introduction of the standard method of cost accounting has been going on for quite a long time. It seems that one of the reasons for this situation is the underestimation by the management of enterprises of the managerial and financial functions of these methods. It is still believed that they are just varieties of general accounting and the solution of emerging issues is given to the accounting personnel of enterprises. But accounting workers face a completely different task - the timely and reliable determination of the total cost of costs, for which traditional calculation methods are quite sufficient. For ordinary accounting, the division of costs into variable and fixed parts is much less important than dividing them into direct and indirect costs. Solving fundamentally new tasks in comparison with financial management, the accountant perceives the task assigned to him in a different way. For him new method accounting is, first of all, a different way of allocating indirect costs between products (or refusing to do so in the case of the direct costing method). And since the introduction of any new method is associated with additional costs, not seeing a significant benefit from such a replacement, the counting worker subconsciously opposes changes that can bring him nothing but additional inconvenience and unnecessary work.

The enterprise is interested in creating a management accounting system that will be focused on controlling opportunity costs. For a number of properties, this system should differ significantly from traditional accounting.

Using the opportunity cost as an example, it becomes obvious influence which at first glance the most abstract provisions of economic theory can (and should) have on the practice of specific enterprises. In the end, the enterprise will suffer quite tangible, real financial losses due to the action of abstract categories, the existence of which the heads of analytical departments did not know or simply did not want to know.

In many cases, opportunity costs are not measurable at all or are estimated very roughly due to the need to take into account the huge number of losses and gains as a result of choosing one or another option of behavior. We present some of these cases. Choosing one strategy of functioning and development, the enterprise loses the opportunity to develop in another direction; the country chooses one direction of socio-economic development, while sacrificing another. In both cases, the alternatives available to the enterprise and the state are very difficult to compare because of their heterogeneity and the impossibility of reducing to a common denominator. It is even more difficult to make a cost, monetary assessment of alternatives when it is necessary to take into account the impact of one or another alternative decision on social welfare. Paliy VF Management accounting of costs and income with elements of financial accounting: Textbook. - M.: Infra-M, 2008..

At practical application The concept of opportunity cost uses the imputation procedure. The concept of "imputation", or attribution (imputation), was one of the first to use the Austrian scientists K. Menger and F. Wieser. It means the procedure for linking certain actions of an economic entity with the benefits that it could receive if it took other actions. To implement the imputation procedure, it is necessary to bring costs and benefits to a comparable form. If the benefit is fixed in the form of some goal, then only the costs are compared. For example, you can get to work by trolleybus or fixed-route taxi. In this case, when evaluating alternatives, the time and cost of travel to work are compared. In other cases, with cost stability (certain budget constraints) benefits, results are compared.

It should be noted that when comparing alternatives, in some cases, incremental cost-benefit ratios should be used instead of averages (additional costs are compared with additional benefits). In medicine, one type of intervention must be compared not only with other types of intervention, but also with non-intervention.

Difficulties arise when using the imputation procedure. The main obstacle lies in the fact that it is far from always possible to reduce to a common denominator all the losses incurred by the subject when making this or that decision. Ivashkevich V.B. Accounting management accounting: a textbook for universities. -- M.: Economist, 2006.

It is believed that opportunity costs may be those arising from not using the best of the available opportunities. But the lost may not be optimal, best opportunity, but, say, the so-called second best, third, etc. Having chosen the optimal option, we lose the opportunities associated with the use of non-optimal options.

Another problem with assessing lost opportunities is its subjective nature. Subjective in some cases are the ranking of alternatives according to the degree of their attractiveness; the choice of costs and benefits (effects), which are taken into account when comparing various options for economic actions, the use of resources.

The processes concerning alternative estimates, as a rule, affect the interests of different economic actors. An increase in the opportunity price of a resource is beneficial for its sellers and disadvantageous for its buyers. The use of a resource in one direction and non-use in another may meet the interests of one group (person) and not meet the interests of another group (person).

In addition, the decision to choose from several alternatives is in some cases taken by a group of people (in economic policy, in an enterprise). Therefore, the problem arises of assessing the costs of lost opportunities for this group and for each of its members individually. The owner of a large stake in an enterprise can block an alternative that, according to him, entails high opportunity costs for the enterprise as a whole, for all shareholders, but in fact only for him. In the future, the subjective nature of the costs of lost opportunities may become the subject of joint research by representatives of the economic, psychological, and sociological sciences.

Given the above and recognizing the difficulty of assessing alternative costs, we can propose an algorithm for estimating the opportunity costs of one of the key economic entities - the enterprise: Trubochkina M. I. Enterprise cost management: tutorial. - M.: Infra-M, 2008.

1) determination of the non-alternative part of the costs of the enterprise (administrative and management expenses, insurance payments, etc.) and the alternative (part of the cost of labor, the purchase of materials, etc.);

2) promotion of alternatives within the alternative part of the costs;

3) comparison of the discounted flows of "expenses-incomes" for each alternative, placing them according to the level of profitability, the effect obtained, etc.;

4) the implementation of the imputation operation and the assessment of losses when choosing a non-optimal alternative.

Thus, the abstract concept of "opportunity costs" gives the manager a powerful, fairly simple, understandable and very practical tool for monitoring the effectiveness of his work: by implementing decisions and projects, the cash inflows for which exceed the cash outflows, he contributes to the growth of the value of the enterprise, thereby properly way it performs its functions. In this regard, there is a need to create an accounting system focused on a more complete and accurate identification of opportunity costs - a management accounting system.

opportunity cost resource economic

Opportunity cost is the term for lost profits when one of the existing alternatives is chosen over another. The amount of lost profits is measured by the utility of the most valuable alternative that was not chosen to replace the other. Thus, opportunity costs occur wherever acceptance is needed. rational decision and there is a need to choose between the available options.

The term was first introduced by the Austrian school economist Friedrich von Wieser in 1914 in his work The Theory of the Social Economy.

Thus, the opportunity cost is the cost of any, measured in terms of the value of the next best alternative, that is withheld. This is a key concept in the economy, providing the most rational and efficient use of limited resources. These costs do not always mean financial costs. They also signify the real value of the forgone product, lost time, pleasure, or any other benefit that provides utility.

There are many examples of opportunity costs. Every person is faced daily with the need to make a choice between available options. For example, a person who wants to watch two interesting TV programs on TV at the same time on different channels, but does not have the opportunity to record one of them, will be forced to watch only one program. Thus, his opportunity cost would be not being able to watch one of the programs. Even if he has the opportunity to record one of the programs while watching the other, even then there will be an opportunity cost equal to the time spent watching the program.

Opportunity costs can also be assessed in the decision-making process in economic activity. For example, if on farming If you can produce 200 tons of barley or 400 tons of rye, then the opportunity cost of producing 200 tons of barley is 400 tons of wheat, which you have to give up.

To see how the opportunity cost can be estimated, let's take Robinson on a desert island as an example. Suppose that near his hut he grows two crops: potatoes and corn. Land plot limited: on one side - the ocean, on the other - the jungle, on the third - rocks, on the fourth - Robinson's hut. Robinson decides to increase corn production. And he can do this in only one way: to increase the area allocated for corn by reducing the area occupied by potatoes. The opportunity cost of producing each subsequent cob of corn in this case can be expressed in terms of potato tubers that Robinson did not receive by using the potato land resource to grow corn.

But this example is for two products. But what if there are dozens, hundreds, thousands of them? Then money comes to the rescue, by means of which all other goods are commensurate.

Opportunity costs can act as the difference between the profit that could be obtained with the most profitable of all alternative ways of using resources, and the profit actually received.

But not all entrepreneurial costs act as opportunity costs. In any way of using resources, the costs that the manufacturer bears in an unconditional manner (for example, registration of an enterprise, rent, etc.) are not alternative. These non-opportunity costs do not participate in the process of economic choice.

Opportunity costs faced by firms include payments to workers, investors, and owners. natural resources. All these payments are made in order to attract factors of production, diverting them from alternative uses.

From the point of view of economics, opportunity costs can be divided into two groups: "explicit" and "implicit".

Explicit costs are opportunity costs that take the form of cash payments to suppliers of factors of production and intermediate products.

Explicit costs include: wages of workers (cash payment to workers as suppliers of a factor of production - work force); cash costs for the purchase or payment for the lease of machine tools, machinery, equipment, buildings, structures (monetary payment to suppliers of capital); payment of transport costs; communal payments(light, gas, water); payment for services of banks, insurance companies; payment of suppliers of material resources (raw materials, semi-finished products, components).

Implicit costs are the opportunity costs of using resources owned by the firm itself, i.e. unpaid expenses.

Implicit costs can be represented as:

- 1. Cash payments that the firm could receive with a more profitable use of its resources. This can also include lost profits ("opportunity costs"); the wages that an entrepreneur could have earned by working elsewhere; interest on capital invested in securities; land rents.

- 2. Normal profit as the minimum remuneration to the entrepreneur, keeping him in the chosen branch of activity.

For example, an entrepreneur engaged in the production of fountain pens considers it sufficient for himself to receive a normal profit of 15% of the invested capital. And if the production of fountain pens gives the entrepreneur less than a normal profit, he will transfer his capital to industries that give at least a normal profit.

3. For the owner of capital, implicit costs are the profit that he could receive by investing his capital not in this, but in some other business (enterprise). For the peasant - the owner of the land - such implicit costs will be the rent that he could receive by renting out his land. For an entrepreneur (including a person engaged in ordinary labor activity), the implicit costs will be the wages that he could receive (for the same time) while working for hire at any firm or enterprise.

Thus, Western economic theory includes the income of the entrepreneur (in Marx it was called the average return on invested capital) in the cost of production. At the same time, such income is considered as a payment for risk, which rewards the entrepreneur and encourages him to keep his financial assets within this enterprise and not divert them for other purposes.

Examples of opportunity costs:

A person who has $15 can buy a CD or a shirt. If he buys the shirt, the opportunity cost is the CD and if he buys the CD, the opportunity cost is the shirt. If there are more choices than two, the opportunity cost is still just one item, never all of them.

When a person comes to the store and is forced to choose between a steak that costs $20 and a trout that costs $40. By choosing the more expensive trout, the opportunity cost is two steaks that could have been purchased with the money spent. And, on the contrary, choosing a steak, the cost will be 0.5 servings of trout.

Opportunity costs are assessed not only in monetary or essential conditions, but also in terms of anything that matters. For example, a person who wishes to watch each of two television programs broadcast at the same time and is unable to record one of them, and therefore can watch only one of the desired programs. Of course, if a person records one program while watching another, then the opportunity cost will be the time the person spends watching the first program rather than the second. In the shop-to-customer situation, the opportunity cost of ordering both meals could be double the extra $40 to buy the second meal, and his reputation as he might be thought of as wealthy enough to spend that much on food. . Also as an option. The family might decide to use the short vacation period to visit Disneyland instead of making home improvements. The opportunity cost here is covered by having happier children, so the bathroom remodel will have to wait another hour.

The consideration of opportunity cost is one of the main differences between the concept of economic cost and cost accounting. Estimating opportunity costs is fundamental to assessing the true cost of any course of action.

Note that the opportunity cost is not the sum of the available alternatives if these alternatives are, in turn, mutually exclusive.

Opportunity costs are sometimes difficult to imagine as a certain amount of rubles or dollars. In a widely and dynamically changing economic environment, it is difficult to choose The best way use of the available resource. In a market economy, this is done by the entrepreneur himself as the organizer of production. Based on his experience and intuition, he determines the effect of a particular direction of resource use. At the same time, income from lost opportunities (and hence the size of opportunity costs) are always hypothetical.

The accounting concept completely ignores the time factor. It estimates the costs based on the results of already completed transactions. And when determining the costs of lost opportunities, it is important to understand that the effect of any option for using a resource can manifest itself in different periods. The choice of an alternative is often associated with the answer to the question, what to prefer: quick profit at the cost of future losses or current losses for the sake of profit in the future? On the one hand, this complicates the assessment of costs. On the other hand, the complexity of the analysis turns into a plus for a more detailed consideration of all aspects of the future project.

The concept of opportunity cost is an effective tool in making effective economic decisions. The assessment of resource costs is carried out here on the basis of comparison with the best of the competing, most effective method use of scarce resources. The centrally controlled system has deprived business entities of independence in making strategic decisions. And that means the possibility of choosing the best alternatives. Themselves central authorities management, even with the help of computers, were unable to calculate optimal structure production for the country. They could not find answers to the two main questions of the economy "what to produce?" and "how to produce?". Therefore, under these conditions, the opportunity cost often resulted in trade deficit and low quality products.

For a market economy, choice and alternativeness are integral features. Resources must be used in an optimal way, then they will bring maximum profit. Saturation with the goods and services that consumers need is a persistent outcome of the opportunity cost of the market system.

Workshop.

Suppose you have 800 rubles. If you decide to spend these 800 rubles. for a football ticket, what is your opportunity cost of going to a football match?

Opportunity costs, costs of lost profits or costs of alternative opportunities - a term denoting lost profits (in a particular case - profit, income) as a result of choosing one of the alternative options for using resources and, thereby, rejecting other opportunities. The amount of lost profit is determined by the utility of the most valuable of the discarded alternatives.

So in order to know the value of the opportunity cost, you need to know the possible uses of these 800 rubles. For example, this amount could be spent on clothes worth 800 rubles, or on products, the total cost of which is also 800 rubles, etc. In this situation, we are faced with a choice and decided to spend 800 rubles. for a football ticket. The cost of purchased goods is the opportunity cost, equal to the cost of services that we sacrifice for the sake of choosing other services. The opportunity cost in this example is the cost of goods and services that we give up in order to purchase a ticket for football.

choice limited resource economic

Opportunity cost is the term for lost profits when one of the existing alternatives is chosen over another. The amount of lost profits is measured by the utility of the most valuable alternative that was not chosen to replace the other. Thus, the law of opportunity costs occurs wherever a rational decision is needed and there is a need to choose between the available options.

The term was first introduced by the Austrian school economist Friedrich von Wieser in 1914 in his work The Theory of the Social Economy.

Determining Opportunity Costs

Thus, the opportunity cost is the cost of any, measured in terms of the value of the next best alternative, that is withheld. This is a key concept in the economy, providing the most rational and efficient use of limited resources. These costs do not always mean financial costs. They also signify the real cost of a product that is abstained from, wasted time, pleasure, or any other benefit that provides utility.

Examples of Opportunity Costs

There are many examples of opportunity costs. Every person is faced daily with the need to make a choice between available options. For example, a person who wants to watch two interesting TV programs on TV at the same time on different channels, but does not have the opportunity to record one of them, will be forced to watch only one program.

Thus, his opportunity cost would be not being able to watch one of the programs. Even if he has the opportunity to record one of the programs while watching the other, even then there will be an opportunity cost equal to the time spent watching the program.

Another example is when a person comes to a restaurant and is forced to choose between a $10 steak and $20 salmon. By choosing the more expensive salmon, the opportunity cost is two steaks that could have been purchased with the money spent. And, on the contrary, choosing a steak, the cost will be 0.5 servings of salmon.

Opportunity costs can also be assessed in the decision-making process in economic activity. For example, if a farm can produce 100 tons of wheat or 200 tons of barley, then the opportunity cost of producing 100 tons of wheat is 200 tons of barley, which has to be discarded.

Topic: Opportunity cost concept

Type of: Test| Size: 27.03K | Downloads: 29 | Added on 02/23/10 at 11:30 | Rating: +2 | More Examinations

University: VZFEI

Year and city: October 2009

Introduction 3

Chapter 1. The concept and types of production costs 4

1.1. Fixed and variable costs 4

1.2. Opportunity cost 6

Chapter 2 Opportunity Cost Concepts 8

2.1. Cost calculation 8

2.2. Applications of the cost concept 17

Chapter 3. Applying the Opportunity Cost Concept 19

Conclusion 21

Tasks 23

Test items 24

References 26

Introduction

The concept of opportunity cost at first glance may seem like a rather exotic abstraction that cannot be used in practice. financial activities. Indeed, why engage in abstract logical constructions, when almost every enterprise has accounting data on the full actual costs of acquiring any asset? There are even frequent disputes about which method of determining costs is more objective: “accounting” or the method of calculating opportunity costs. The very formulation of such a question does not seem quite correct. The main difference between these methods is not in "accuracy" and "objectivity", but in their purpose. Analyzing the financial statements of an enterprise, any researcher without a shadow of a doubt uses accounting data to calculate the liquidity ratio or the availability of their own working capital. Of the same interest are indicators financial statements for tax inspectors, auditors, auditors who check the activities of the enterprise. Common to all these categories of users of reporting information is the desire to understand the transactions that have already been completed.

The relevance of the topic chosen for the study lies in the importance of applying the concept of opportunity costs.

The purpose of the control work is to study planning and cost accounting, which become important in management decisions. To achieve this goal, the following tasks are solved:

- Analyze the types of costs;

- Consider the concept of opportunity cost;

- To study the application of the concept of opportunity cost.

The subject of the study is the calculation of opportunity costs, forms of manifestation of the concept of opportunity costs.

Chapter 1. The concept and types of production costs

1.1. Fixed and variable costs

Speaking about production costs, K. Marx considered the process of formation of costs directly according to their main elements in manufacturing process. He abstracted from the problem of price fluctuation around value. In addition, in the twentieth century, it became necessary to determine the changes in costs depending on the amount of output produced.

Modern concepts of costs largely take into account both of the above points. In the center of the classification of costs is the relationship between the volume of production and costs, the price of a given type of goods. Costs are divided into independent and dependent on the volume of production.

Fixed costs do not depend on the size of production, they exist even at zero volume of production. These are the previous obligations of the enterprise (interest on loans, etc.), taxes, depreciation, payment for security, rent, equipment maintenance costs at zero production volume, salaries of management personnel, etc. Variable costs depend on the quantity of products produced, they consist of the costs of raw materials, materials, wages to workers, etc. The sum of fixed and variable costs forms gross costs - the amount of cash costs for the production of a certain type of product. To measure the cost of producing a unit of output, the categories of average, average fixed and average variable costs are used. The average cost is equal to the quotient of dividing the total cost by the amount of output produced. Average fixed costs are determined by dividing the fixed costs by the quantity of output produced. Average variable costs are formed by dividing the variable costs by the amount of output produced.

To achieve maximum profit, you need to determine the required amount of output. Tool economic analysis is the category of marginal cost. marginal cost is the incremental cost of producing each additional unit of output over a given output. They are calculated by subtracting adjacent gross costs.

1.2. opportunity cost

In real production activities it is necessary to take into account not only the actual monetary costs, but also the opportunity costs. The latter arise because of the possibility of choosing between certain economic solutions. For example, the owner of an enterprise can spend the available money in various ways: he can use it to expand production or spend it on personal consumption, etc. Measurement of opportunity costs is necessary not only for market relations, but also for objects that are not goods. In an unregulated commodity market, the opportunity cost will be equal to the current market price. this moment market price. If there are several different (usually close) prices on the market, then the opportunity cost of selling the product at, naturally, the highest price offered to the seller by buyers will be equal to the highest of all remaining (except the highest) prices offered.

Earlier in the USSR, the construction of hydroelectric power stations (HPPs) on rivers flowing through the plains was widespread. It is possible to receive income from the production of electricity during the construction of a dam, the creation of a reservoir and the installation of a hydroelectric power station. In case of refusal of this construction, it is possible with the help of the released cash and material resources earn income from conducting intensive methods of coastal Agriculture, fishing, forestry and other economic activities on lands that can be turned into the bottom of the hydroelectric reservoir. The total economic costs of obtaining electricity will be equal to the sum of the costs of building a hydroelectric power station and the valuation of the possible volume of production from intensive economic activity on flooded lands (opportunity costs). The total economic costs of any kind of economic activity should include, in addition to the usual monetary and material, also opportunity costs, covering valuation the best possible alternative decision on the use of available resources (labor, money, material, etc.).

Chapter 2 Opportunity Cost Concepts

2.1. Cost calculation

Production costs are expenses, cash expenditures that must be made to create a product. For an enterprise (firm), they act as payment for the acquired factors of production.

Such expenses cover payment for materials (raw materials, fuel, electricity), wages of employees, depreciation, costs associated with production management. When selling goods, the entrepreneur receives cash proceeds. One part of it compensates for the costs of production (i.e., the cost of money associated with the production of goods), the other gives a profit, that for which production is organized. This means that the cost of production is less than the cost of goods by the amount of profit

Simplifying the concept, we can say that the costs of the enterprise are understood as what it costs to produce products.

For financial management, data on the future cash flows of the enterprise arising from the adoption of a particular management decision are of the greatest interest. In the process of control, the control subsystem must influence the control object. The actual cash flows reflected in the accounting of the enterprise result from previously made management decisions. Information about these flows is an element of feedback between the subject and the control object. It has significant value in substantiating managerial decisions, but the result of these decisions will be to change future, not today's, cash flows. To assess the financial and economic efficiency of the decisions made, it is necessary to compare future cash inflows with future outflows due to the adoption and implementation of these decisions.

For example, in order to make a decision on the release of a new type of product, one should calculate the amount of costs that an enterprise will incur in the production and sale of a new product, and compare this value with the expected income from its sale. At first glance, it may seem quite natural to use the calculation of the total cost of one product for these purposes, and, multiplying its amount by the planned sales volume, get the total cost of new products. However, this approach overlooks an important circumstance: a significant part of the total costs is associated with cash flows that took place in the past, even before the decision was made. The implementation of the decision will have no impact on the related cash flows in the future. If it is planned to use the stocks of materials already available at the enterprise for the production of a new product, and their available quantity is sufficient to cover the entire planned need and no new purchases of these materials are expected, then it is not known how the costs of purchasing these materials are related to the release of a new product and what real cash outflows will be incurred by the enterprise, using these materials in the process of implementing this decision.

In connection with these unknown quantities, the concept of opportunity costs is widely used in financial management.

In economic theory, opportunity (imputed or economic) costs are understood as the amount (cost) of other products that should be abandoned or sacrificed in order to get some amount of this product. It can be argued that the material costs for the production of new products for the enterprise will be equal to the amount that it could earn by selling the stock of materials, since the enterprise has no other alternative to using them.

A more general definition of economic cost is the payment that a firm is required to make, or the income that a firm is required to provide, to a supplier of resources in order to divert those resources away from use in alternative industries. The release of a new product will be appropriate for the enterprise if the price offered by the buyer for it will cover the opportunity costs of both raw materials and materials, and all other resources spent on the production of the product.

The orientation of financial management to cash flows generated by management decisions allows us to define opportunity costs as the amount of cash outflow that will occur as a result of making a decision. The decision to launch a new product in production entails a loss of revenue from the sale of materials available at the enterprise. The cost of these materials at the prices of their possible sale will be the amount of material costs, which must be taken into account when justifying the corresponding decision.

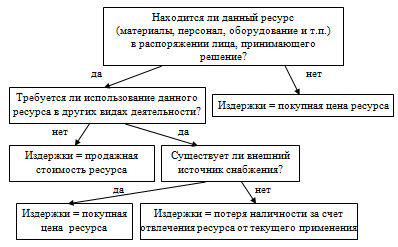

Distinguish between internal and external opportunity costs. If the company did not have stock necessary materials, it would have to purchase them, incurring direct cash costs. In this case, one speaks of external opportunity costs. The enterprise will have to incur the same costs if, for the production of a new product, it needs to hire an additional number of employees of appropriate qualifications. The wages (with all accruals on it) of these workers will represent an additional cash outflow, the value of which will characterize the level of external opportunity costs.

If you plan to use internal resource, already available at the enterprise, and paid earlier, regardless of the decision made, then they talk about internal costs. Their value is also determined by the size of future cash outflows, but the nature of these outflows will be different. As a rule, we will not talk about cash costs, but about the loss of additional income. In the case of inventories, this is the price of their possible sale. If, instead of hiring new employees, the enterprise wants to use the labor of existing personnel in the production of a new product, then the value of internal opportunity costs will be determined by the amount of income that the enterprise will lose as a result of distracting employees from their previous occupations.

The total opportunity cost of any management decision is equal to the sum of its internal and external opportunity costs. Better assimilation of the concept of opportunity costs is facilitated by the use of the flowchart proposed by the English scientist B. Ryan:

Figure - Decision-making algorithm for opportunity costs

Let us consider an example of using this reasoning scheme in the course of estimating the value of opportunity costs. The enterprise received an order for the sale of a batch of products in the amount of 5000 pieces at a price (without VAT) of 40 rubles per 1 piece. This product has been mastered by the enterprise, but in recent times its release was not carried out due to lack of demand. For its manufacture, a single type of material is required, the stock of which in the amount of 2.5 tons is available at the enterprise and must be renewed in the same volume. The purchase price of the material at the time of the last purchase was 30 rubles. per 1 kg (excluding VAT), but currently it has increased by 5%. For the production of 1 product, 0.5 kg of this material is required. The labor intensity of 1 product is 0.4 standard hours, hourly tariff rate the main workers employed in its production (including social charges) - 25 rubles. To complete the order within 10 days, it is necessary to attract 25 workers for this period, of which 10 will be re-hired under a labor agreement for 10 days, 10 will be used from among full-time employees temporarily idle due to lack of work, 5 will be distracted from others works. Labor productivity and wages for each of the 25 workers will be the same. General production costs of the enterprise are 100% of the main wages key production workers; general business expenses - 50% of the same base. Non-manufacturing (commercial) expenses amount to 5% of the production cost of products sold.

With such data, planning department the enterprise made the following calculation of the total planned cost of products (Table 1).

Planned calculation of the full cost of 1 product, rub.

Table 1.

|

Expenditures |

||

|

1. Main materials |

||

|

2. Basic salary (with accruals) |

||

|

3. General production costs |

||

|

4. General business expenses |

||

|

Production cost of 1 product |

||

|

5. Non-production (commercial) expenses |

||

|

Full cost of 1 product |

It follows from the calculation that on each product the enterprise will lose 2 rubles (42 - 40), which, based on the entire output, will be 10 thousand rubles. (2 x 5000) loss. It is obvious that the enterprise should not agree to the execution of an order that brings him losses. However, by calculating the opportunity costs for this order, you can get a different result. First of all, it is necessary to study additional initial data: during the downtime, the enterprise accrues wages at the rate of 30 rubles per employee. in a day. 5 people who are planned to be diverted from their work receive 125 rubles each. in a day. Transferring them to another job for 10 days will mean a loss of income for the enterprise in the amount of 35 thousand rubles, due to a decrease in the output of their products. In connection with the implementation of a new order, not all indirect costs of the enterprise will increase, but only their variable part, which is calculated at the following rates: production overheads - 10 rubles. for each additional standard hour of the scope of work; variable selling expenses - 2 rubles, for each additional product sold.

Given these conditions, the calculation of opportunity costs will have the following form:

1. Calculation material costs. At the time of the decision, the enterprise had the necessary amount of materials that it did not intend to use for another purpose. The decision to fulfill the order could not affect their cost, so the actual costs of purchasing already existing materials should not be taken into account. The company plans to renew this stock at a higher price of 31.5 rubles. per 1 kg (30 + 0.05 x 30), therefore, the opportunity costs for the purchase of the same amount of materials will amount to 78.75 thousand rubles. (31.5 x 2500). These costs are associated with the internal reallocation of resources, they do not follow directly from the decision to release new products, since the materials were already in the warehouse of the enterprise, so they should be attributed to internal opportunity costs.

2. Calculation of the cost of wages. The wages of 10 newly recruited temporary workers are fully conditioned by this decision. Based on an 8-hour working day, the amount of payment for their work for 10 days of work will be 20 thousand rubles. (10 people x 8 hours x 10 days x 25 rubles). Unloaded full-time workers currently receive time wages at the rate of 30 rubles. in a day. Therefore, the opportunity cost of their wages will amount to 17 thousand rubles. (10 people x 8 hours x 10 days x 25 rubles - 10 people x 10 days x 30 rubles). The distraction of another 5 full-time employees from the work performed will entail a loss of income of the enterprise by 35 thousand rubles, this amount should be taken into account as part of opportunity costs. At their previous job, their salary was 125 rubles. per day, therefore, the total cost of their wages will be 38,750 rubles. (5 people x 8 hours x 10 days x 25 rubles - 5 people x 10 days x 125 rubles + 35,000 rubles). In total, the enterprise's opportunity costs for wages will be equal to 75,750 rubles. Of these, additional cash outflows due to the decision under consideration (external costs) will amount to 50 thousand rubles. (25 people x 8 hours x 10 days x 25 rubles); losses associated with the diversion of resources (internal costs) will amount to 25,750 rubles. (35,000 rubles - 10 people x 10 days x 30 rubles - 5 people x 10 days x 125 rubles).

3. Calculation of overhead and commercial expenses. The labor intensity of the additional production of 5000 products will be 2000 standard hours (5000 x 0.4). Therefore, the increase in variable overhead production costs will be equal to 20 thousand rubles. (2000 x 10). The increase in variable commercial expenses will be 10 thousand rubles. (5000 x 2). These costs are decision-driven, so they are external opportunity costs. Fixed indirect costs will remain unchanged in any case, so they should not be included in the opportunity cost calculation for this solution.

Summarizing the performed calculations, we construct Table 2.

Calculation of opportunity costs, thousand rubles

table 2

|

Expense items |

opportunity cost |

||

|

internal |

|||

|

1. Direct materials |

|||

|

3. Variable manufacturing overheads |

|||

|

4. Variable selling expenses |

|||

|

Total opportunity cost |

|||

Thus, the total opportunity costs will amount to 184.5 thousand rubles, which is 15.5 thousand rubles lower than the cost of selling 5000 products (200 thousand rubles). It turns out that it is beneficial for the enterprise to agree to the execution of the order, since the proceeds received will not only cover all the costs associated with it, but will also provide a contribution to cover its fixed costs in the amount of 15.5 thousand rubles.

However, the amount of fixed costs of the entire enterprise is much higher than 15.5 thousand rubles. And therefore, when planning its activities, an enterprise must form such a portfolio of orders so that their totality covers all fixed costs and ensures profit. If this cannot be achieved, then it is necessary to reduce fixed costs that are not directly related to the production and commercial activities of the enterprise. It does not have the luxury of investing its financial resources in capacity development that does not bring real returns. In any case, we are talking about qualitatively different decisions that have nothing to do with the decision to fulfill a specific order. If the company has a choice, then, of course, one should prefer a more profitable option that provides maximum coverage of fixed costs. But the lack of choice cannot be a reason for not producing products whose price is higher than their opportunity cost.

By refusing to manufacture products that fully cover their opportunity costs in the hope of obtaining better orders that pay for the full cost of each product, the company loses real cash inflows from hands, chasing expected higher cash inflows in the future. Such behavior is contraindicated both for a financial manager and for any businessman. Business owners (investors) pay their managers the only service - the real increase in invested capital. A manager should not turn down the opportunity to secure at least a minimal capital increase if he does not have a real alternative opportunity for a more profitable use of the assets.

2.2. Forms of application of the concept of costs

The following forms of practical manifestation of the considered concept of opportunity costs can be distinguished:

1. When justifying financial decisions, one should focus primarily on the cash flows generated by these decisions. Here it is appropriate to recall again the expression of B. Ryan, modestly defined by him as "Ryan's Second Law": "Costs and incomes arise only at those moments when cash flows cross the boundaries of the enterprise." Without questioning the value and importance of full costing, financial management operates with somewhat different concepts, the central among which is cash flow.

2. Those and only those cash flows that are directly related to this decision should be taken into account. Receipts and expenditures of funds, regardless of the time of their occurrence, not related to the decision being made, should not be taken into account. In other words, financial management works with incremental cash flows, and the opportunity costs considered in it are marginal. If, as a result of a decision to release a new product, it is necessary to hire additional security guards to the staff of the enterprise, then the marginal costs of maintaining new security workers should be included in the cost of the product being mastered, while the costs of maintaining the guards in the same size are not relevant to this decision and in opportunity costs should not be included.

3. The decision taken cannot affect the expenses already incurred or the income received earlier. Therefore, justifying this decision, the financial manager should take into account only future cash flows. All past payments and receipts, including the cost of purchasing equipment, are of a historical nature, they can no longer be avoided or prevented. Therefore, in financial calculations such an element of costs as depreciation of fixed assets is not involved.

Chapter 3. Applying the Opportunity Cost Concept

The application of the concept of opportunity costs poses serious challenges for the information subsystem of financial management. It is obvious that the data of traditional accounting alone is not enough in this case. There is a need to create an accounting system focused on a more complete and accurate identification of opportunity costs - a management accounting system. The cornerstone of such a system is the division of all expenses of the enterprise into conditionally fixed and variable parts in relation to the volume of output (sales) of products.

Planning and accounting for costs in this context makes it possible to more closely link them with the consequences of specific management decisions, to exclude the possibility of “overlapping” the financial results of this decision with the influence of factors unrelated to it (for example, general factory overhead costs).

Another distinguishing feature of such systems is the wide coverage of enterprise costs by rationing. This allows you to more accurately predict future cash inflows and outflows.

The third feature of management accounting systems is the personification of information, the linking of accounting objects with the areas of responsibility of specific managers, which makes it possible to even more clearly delineate the costs that depend on specific decisions from all other costs that are not related to it.

The listed features are reflected in such accounting systems as the normative method of accounting for production costs (standard-cost system), accounting for variable costs (direct costing), accounting for cost centers, profit centers and responsibility centers.

At Russian enterprises, all these systems take root rather slowly, despite the fact that the introduction of the standard method of cost accounting, for example, has been going on for over 60 years. It seems that one of the reasons for this situation is the underestimation by the management of enterprises of the managerial and financial functions of these methods. It is still believed that they are just varieties of general accounting and the solution of emerging issues is at the mercy of the accounting personnel of enterprises. But the accounting workers are faced with a completely different task - the timely and reliable determination of the total cost of historical costs, for which traditional calculation methods are quite sufficient.

For ordinary accounting, the division of costs into variable and fixed parts is much less important than dividing them into direct and indirect costs. Solving fundamentally different tasks in comparison with financial management, the accountant perceives the task assigned to him in a different way. For him, the new method of accounting is, first of all, a different way of allocating indirect costs between products (or refusing to do so in the case of the direct costing method). And since the introduction of any new method is associated with additional costs, not seeing a significant benefit from such a replacement, the counting worker subconsciously opposes changes that can bring him nothing but additional inconvenience and unnecessary work.

Thus, being one of the main consumers of general (financial) accounting information, financial management is also interested in creating a management accounting system focused on controlling alternative costs. According to a number of properties, this system should differ significantly from traditional accounting, therefore, when creating it, the requirements and needs, first of all, of financial management should be taken into account. It is quite possible that even the organizational status of the relevant unit may differ from the status of general accounting and its operational activities, the greater impact will be financial director, but not Chief Accountant enterprises.

Conclusion

Each production unit (enterprise) of any society seeks to obtain the greatest possible income from its activities. Any enterprise tries not only to sell its goods at a profitable high price, but also to reduce its costs for production and sale of products. If the first source of increasing the income of the enterprise largely depends on the external conditions of the enterprise, then the second - almost exclusively on the enterprise itself, more precisely, on the degree of efficiency of the organization of the production process and the subsequent sale of manufactured goods.

Many economists have made significant contribution in the study of costs. Production costs are understood as the costs of wages, raw materials and materials, this also includes depreciation of labor instruments, etc. Production costs are the costs of production that the organizers of the enterprise must incur in order to create goods and then make a profit. In the cost of a unit of goods, the cost of production is one of its two parts. Production costs are less than the cost of goods by the amount of profit.

The financial manager is faced with the task of designing a future financial transaction, assessing as accurately as possible all the possible benefits and losses associated with this particular operation. At the same time, he in no way rejects the already available “historical” data, on the contrary, the analysis of financial statements is one of the most important tasks of financial management. However, in order to justify financial decisions aimed at obtaining future results, appropriate tools with specific properties are needed. The concept of opportunity costs forms the theoretical basis of such tools, so it is often not presented in an explicit form, and many practitioners, performing financial calculations, use this concept without even knowing it exists.

Tasks

Task 1

The company's profit before interest and taxes amounted to 4 million rubles, the amount of interest on the loan was 1.5 million rubles, the income tax rate was 20%. Evaluate the effectiveness of the organization's borrowing policy based on the following balance sheet data:

|

Asset, million rubles |

Liabilities, million rubles |

||

|

Buildings and constructions |

Equity |

||

|

Borrowed capital, including: Short long term |

|||

|

Inventory |

|||

|

Accounts receivable |

|||

|

Cash |

|||

ER = (4.0: 14) * 100% = 28.6%

SRSP \u003d (1.5: 6) * 100% \u003d 25%

EDR \u003d (1 - 0.2) (28.6 - 25) \u003d 6\8 \u003d 2.16%

Task 2

The depositor placed 40 thousand rubles in the bank for 4 years. Simple interest is charged: in the first year - at a discount rate of 8%, in the second - 7%, in the third - 9%, in the fourth - 7%. Determine the future value of the investment by the end of the fourth year.

S \u003d 40000 (1 + 0.08 + 0.07 + 0.09 + +0.07) \u003d 52.4 thousand rubles.

Test tasks

1. The level of risk of loss of profit is greater if:

1. natural volume of sales decreases and prices rise at the same time

2. natural volume of sales is growing and at the same time prices are falling

3. Prices and volume of sales decrease

Rationale:

Demand for products falls, and price increases reduce demand even more. and all this reduces the volume of sales.

According to the mechanism of operating leverage, any decrease in the volume of sales will further reduce the size of gross operating profit.

2. Bank deposit for the same period increases more when interest is applied

1. simple

2. complex

Rationale:

A deposit in the amount of 50 thousand rubles was accepted. for a period of 90 days at a rate of 10.5 percent per annum. Calculate the amount of a bank deposit using simple and compound interest.

Simple interest:

Sp \u003d 50000 x 10.5 x 90 / 365 / 100 \u003d 1294.52

S = 50000 + 1294.52 = 51294.52

Compound interest (with interest compounded every 30 days)

S \u003d 50000 x (1 + 10.5 x 30 / 365 / 100) 3 \u003d 51305.72

Sp \u003d 50000 x [(1 + 10.5 x 30 / 365 / 100) 3 - 1) \u003d 1305.72

As a result, for 90 days, compound interest amounted to 11.2 rubles. more.

3. Operating lever evaluates:

1. cost of products sold

2. sales proceeds

3. degree of profitability of sales

4. a measure of profit sensitivity to changes in prices and sales volumes

Rationale.

Operating leverage, by definition, shows how many times operating profit changes with an increase in revenue.

4. The elements of risk classification according to the level of financial losses are:

1. acceptable risk

2. external risk

3. tax risk

4. simple risk

Rationale:

According to the level of financial losses, the risk is divided into: acceptable, critical, catastrophic.

External risk is a classification according to the sphere of occurrence.

Tax risk is a classification by types of financial risks.

Simple risk is a classification according to the possibility of further classification.

5. Enterprises No. 1 and No. 2 have equal variable costs and equal profit from the sale, but the sales revenue in enterprise No. 1 is higher than in enterprise No. 2. The critical volume of sales will be greater in the enterprise:

1. № 1

Rationale.

The critical sales volume can be defined as the sales volume at which marginal profit equals fixed costs. Enterprise No. 1 has higher sales revenue, therefore, the critical sales volume is also higher (ceteris paribus).

List of used literature

- Kovalev V.V. Introduction to financial management. - M.: Finance and statistics, 2007. - 768 p.

Friends! You have a unique opportunity to help students like you! If our site helped you find the right job, then you certainly understand how the work you added can make the work of others easier.

If the Control Work, in your opinion, is of poor quality, or you have already met this work, let us know about it.

We also recommend

mafia style party invitations

mafia style party invitations

Gangster themed kids birthday party

Gangster themed kids birthday party

Games for a corporate party in nature in the summer are cool

Games for a corporate party in nature in the summer are cool

Presentation - domestic and wild birds Educational presentation "Such different birds" for children of younger preschool

Presentation - domestic and wild birds Educational presentation "Such different birds" for children of younger preschool

How to write a report: an example and recommendations How to write a thematically informative report

How to write a report: an example and recommendations How to write a thematically informative report

"April 1 - April Fool's Day" methodological development on the topic Scenarios for April Fool's Day in the House of Culture

"April 1 - April Fool's Day" methodological development on the topic Scenarios for April Fool's Day in the House of Culture